- Case-Based Roundtable

- General Dermatology

- Eczema

- Chronic Hand Eczema

- Alopecia

- Aesthetics

- Vitiligo

- COVID-19

- Actinic Keratosis

- Precision Medicine and Biologics

- Rare Disease

- Wound Care

- Rosacea

- Psoriasis

- Psoriatic Arthritis

- Atopic Dermatitis

- Melasma

- NP and PA

- Skin Cancer

- Hidradenitis Suppurativa

- Drug Watch

- Pigmentary Disorders

- Acne

- Pediatric Dermatology

- Practice Management

- Prurigo Nodularis

- Buy-and-Bill

Article

Avoid common mistakes when planning for next year's new tax laws

Changes in tax laws can catch successful people off guard. With most physicians so busy worrying about potential reimbursement reductions, they don't have the time to address the important challenge of establishing a tax-wise estate plan for their families.

Key Points

Changes in tax laws can catch successful people off guard. With most physicians so busy worrying about potential reimbursement reductions, they don't have the time to address the important challenge of establishing a tax-wise estate plan for their families.

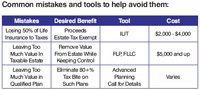

In our experience, fewer than 5 percent of doctors have an adequate estate plan in place when we meet. This upcoming tax law change will create even more shortfalls in most doctors' planning. We see that physicians typically make one or more of these three common mistakes:

Fortunately, there are a few simple tools doctors can use to help circumvent such mistakes and allow their families to avoid the unnecessary costs that come with poor estate planning.

One common misconception most physicians have about life insurance is that all insurance proceeds are exempt from estate taxes. This idea is not true. Life insurance proceeds are exempt from income tax, but they are subject to both federal and state estate taxes. Federal estate tax rates, now and under current proposals, would likely be about 45 to 50 percent, and surviving family members also would need to pay individual states' estate and inheritance taxes on these proceeds. Physicians' family members should not lose a large percentage of the life insurance policy proceeds when a simple legal tool can solve this problem and provide better lawsuit protection for insurance beneficiaries.

A good way to avoid losing a significant portion of life insurance proceeds - or possibly any proceeds at all - is to establish an irrevocable life insurance trust (ILIT). As the name implies, an ILIT is a trust that owns a life insurance policy. The ILIT can save a physician estate taxes because it, rather than the physician personally, owns the life insurance policy. Since the policy is not held in the doctor's name, the policy proceeds will not be part of his or her net estate at the time of death, as long as the physician survives three years from the time of the transfer to the trust. The proceeds, therefore, are not subject to estate taxes.

Such a trust can save a physician's family a great deal of money. An ILIT is indispensable for life insurance policies owned for estate-planning purposes. This type of ownership is ideal for estate planning but not for those tax-savvy investors who are using life insurance to generate tax-efficient retirement wealth.

The ILIT gives the insured much more control over what happens to the policy proceeds than he or she would get from a beneficiary designation of an insurance policy. With an insurance policy alone, the only decisions the insured can make is to whom to leave the proceeds and whether to pay all the money out in a lump sum or over a specific period of time (with an annuity payout option).

With an ILIT, however, the insured can control not only who receives the proceeds but also exactly what happens to the funds when he or she dies. The ILIT can require the trustees to pay the beneficiaries immediately in a lump sum or pay them over months or years, with more creativity than a beneficiary designation offers. The insured also can incorporate spendthrift provisions and anti-alienation provisions to protect the surviving family members against their own financial problems or their spouse's financial woes. The ILIT offers tax reduction, asset protection and planning creativity that cannot be achieved with a simple beneficiary designation.

For these reasons, every physician should consider an ILIT when purchasing a life insurance policy that is to be used as part of a well-crafted estate plan.

For physicians who have already purchased a life insurance policy or who are currently making payments on an existing policy, it is not too late to establish an ILIT. A policy can be transferred to an ILIT at any time. There may be some gift-tax issues associated with such a transfer, but these issues are likely to be minor compared with the potential tax savings a physician's family could enjoy.